This article is the second in a series developed by Three Pillars Consulting on product-level emissions reporting within the petrochemical sector and co-published with the Gulf Petrochemicals & Chemicals Association (GPCA). The first article, Emissions Disclosures: The Shift to Product-Carbon Footprinting, introduced the distinction between corporate-level and product-level GHG reporting, and explained why product carbon footprints (PCFs) are increasingly central to procurement decisions, regulatory compliance, and market access. This article explores how the energy mix in the electricity grid influences Scope 2 emissions reporting and PCF values.

Recap: From corporate inventories to product carbon footprints

Article 1 of this series clarified the distinction between corporate-level and product-level greenhouse gas (GHG) reporting. Corporate-level reporting, governed by standards such as the GHG Protocol Corporate Standard and ISO 14064-1, measures a company’s total Scope 1, Scope 2, and (optionally) Scope 3 emissions in absolute terms. While essential for tracking overall performance and setting net-zero targets, this approach has certain limitations such as not allowing for meaningful benchmarking between companies.

Product carbon footprints (PCFs), by contrast, normalize emissions relative to a defined functional unit of production (e.g. one ton of ammonia). Governed by standards such as ISO 14067 and the GHG Protocol Product Standard, PCFs integrate emissions across defined life-cycle stages and, critically, require the attribution of upstream material emissions (including feedstocks) that are often optional under corporate reporting. This style of accounting is becoming more common across regulatory frameworks (e.g. CBAM) and procurement criteria across many sectors and industries.

A dimension of the PCF calculation that deserves particular attention is the contribution of electricity-based Scope 2 emissions to the overall PCF result. This is the focus of the present article.

How much do petrochemical products depend on electricity?

GPCA members collectively produce a wide range of petrochemical and chemical products, including ammonia and urea (the dominant nitrogen fertilizer products), methanol, ethylene and propylene (olefins produced via steam cracking), polyethylene and polypropylene, aromatics (benzene, toluene, xylenes), and specialty chemicals such as chlor-alkali products and industrial gases.

The degree to which each of these products depends on electricity, versus direct fuel combustion for heat and feedstock, varies considerably. Steam crackers, which produce ethylene and propylene, are dominated by thermal energy (process heat from combustion), meaning that electricity is a secondary but non-negligible contributor. Polymer plants (PE, PP) downstream crackers are comparatively more electricity-intensive, as compressors, reactors, and pelletizing equipment are electrically driven. Ammonia plants are predominantly gas-fired (for the steam methane reformation step and the Haber-Bosch synthesis loop), but electricity drives auxiliary systems, refrigeration compressors, and air separation. Chlor-alkali plants represent an extreme case: the electrolytic splitting of brine to produce chlorine and caustic soda is almost entirely electricity-powered, making the chlor-alkali process one of the most electricity-intensive in the entire chemicals sector.

While the energy mix varies by process, production across this portfolio is universally energy-intensive, drawing on a combination of direct fuel combustion for heat and feedstock, and electricity sourced from the grid. The balance between these two differs by product, but grid electricity is a meaningful contributor across almost all of them, and in some cases, such as chlor-alkali, it is the dominant energy source. This means that for GCC exporters, the carbon intensity of the local grid directly feeds into the embedded emissions of their products and, by extension, their exposure to mechanisms like The EU Carbon Border Adjustment Mechanism (CBAM).

GCC grids: Energy mix and emissions intensities

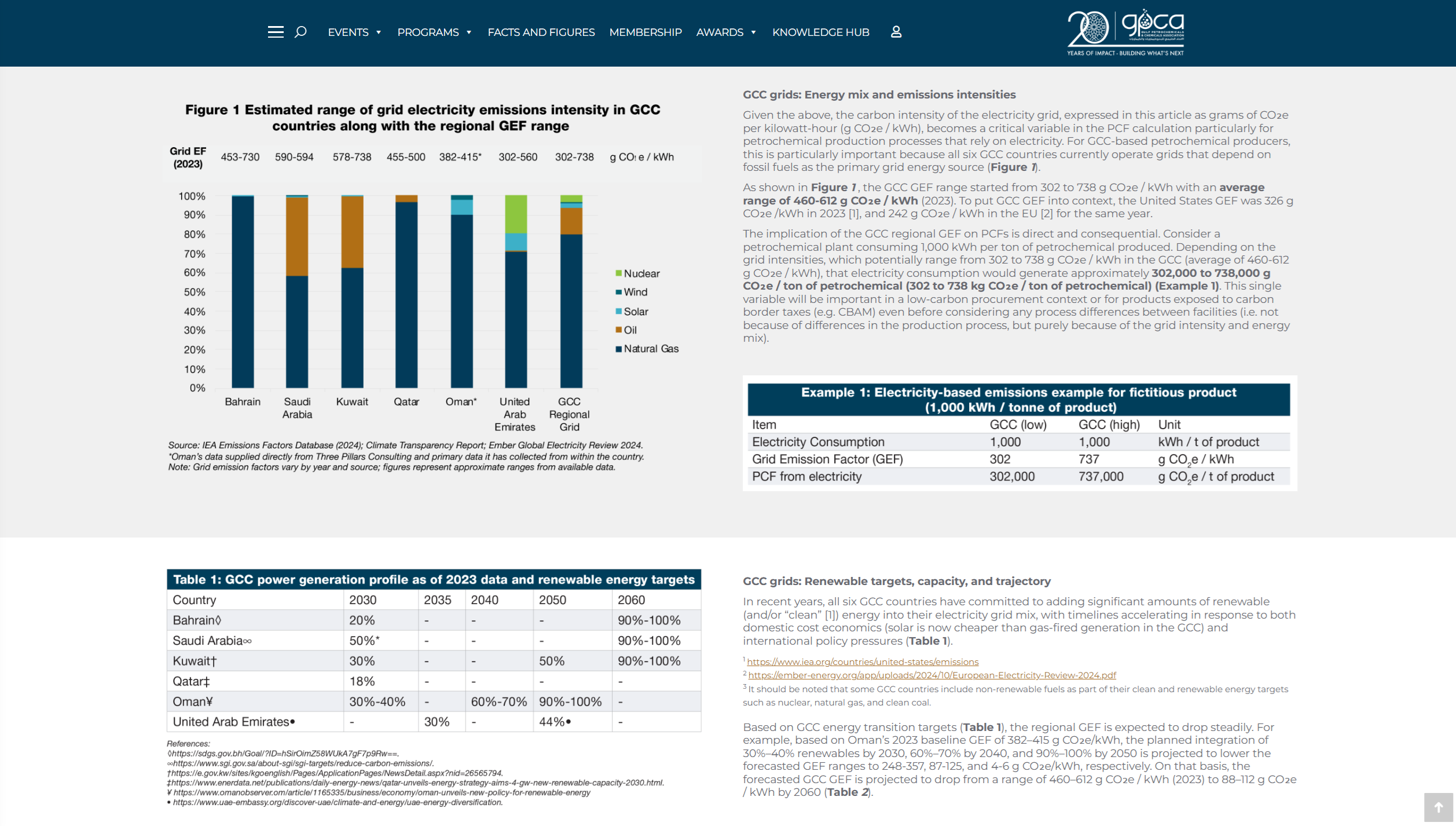

Given the above, the carbon intensity of the electricity grid, expressed in this article as grams of CO₂e per kilowatt-hour (g CO₂e / kWh), becomes a critical variable in the PCF calculation particularly for petrochemical production processes that rely on electricity. For GCC-based petrochemical producers, this is particularly important because all six GCC countries currently operate grids that depend on fossil fuels as the primary grid energy source (Figure 1).

As shown in Figure 1 , the GCC GEF range started from 302 to 738 g CO₂e / kWh with an average range of 460-612 g CO₂e / kWh (2023). To put GCC GEF into context, the United States GEF was 326 g CO₂e /kWh in 2023 [1], and 242 g CO₂e / kWh in the EU [2] for the same year.

The implication of the GCC regional GEF on PCFs is direct and consequential. Consider a petrochemical plant consuming 1,000 kWh per ton of petrochemical produced. Depending on the grid intensities, which potentially range from 302 to 738 g CO₂e / kWh in the GCC (average of 460-612 g CO₂e / kWh), that electricity consumption would generate approximately 302,000 to 738,000 g CO₂e / ton of petrochemical (302 to 738 kg CO₂e / ton of petrochemical) (Example 1).

This single variable will be important in a low-carbon procurement context or for products exposed to carbon border taxes (e.g. CBAM) even before considering any process differences between facilities (i.e. not because of differences in the production process, but purely because of the grid intensity and energy mix).

GCC grids: Renewable targets, capacity, and trajectory

In recent years, all six GCC countries have committed to adding significant amounts of renewable (and/or “clean” [1]) energy into their electricity grid mix, with timelines accelerating in response to both domestic cost economics (solar is now cheaper than gas-fired generation in the GCC) and international policy pressures (Table 1).

1 https://www.iea.org/countries/united-states/emissions

2 https://ember-energy.org/app/uploads/2024/10/European-Electricity-Review-2024.pdf

3 It should be noted that some GCC countries include non-renewable fuels as part of their clean and renewable energy targets such as nuclear, natural gas, and clean coal.

Based on GCC energy transition targets (Table 1), the regional GEF is expected to drop steadily. For example, based on Oman’s 2023 baseline GEF of 382–415 g CO₂e/kWh, the planned integration of 30%–40% renewables by 2030, 60%–70% by 2040, and 90%–100% by 2050 is projected to lower the forecasted GEF ranges to 248-357, 87-125, and 4-6 g CO₂e/kWh, respectively. On that basis, the forecasted GCC GEF is projected to drop from a range of 460–612 g CO₂e / kWh (2023) to 88–112 g CO₂e / kWh by 2060 (Table 2).

On a country level, Oman is on a path to reach the region’s lowest individual intensity, forecasted at 4–6 g CO₂e / kWh by 2050. Kuwait and Saudi Arabia follow this trajectory, aiming for 10–15 g CO₂e / kWh by 2060 as the Shagaya Renewable Energy Park[1]. While the UAE utilizes a combination of solar and nuclear energy from the Barakah Plant [2] to meet its 2050 Net Zero goal, Qatar maintains a higher relative long-term forecast of 373–410 g CO₂e / kWh. Collectively, these pathways show a regional transition where Oman and the UAE reach near-zero or net-zero grid states by 2050, with Saudi Arabia, Kuwait, and Bahrain aligning their decarbonization results with 2060 (Table 2).

5 https://pris.iaea.org/PRIS/CountryStatistics/CountryDetails.aspx?current=AE

Why this matters: CBAM example and embedded electricity emissions

Carbon intensity values are still largely reported on a voluntary basis, driven by industry standards, shifting expectations in best practices, and end-user demands. However, the regulatory landscape is now shifting towards compliance-based reporting of carbon intensities such as what is being done under the EU’s CBAM.

CBAM entered its definitive financial enforcement phase on 1 January 2026 and now requires EU importers of covered goods to report and pay for embedded carbon. As of 2026, CBAM covers cement, iron and steel, aluminium, fertilizers (including ammonia and urea), electricity, and hydrogen. This levy specifically includes Scope 2 indirect emissions from electricity for certain products, making it a critical concern for GCC producers of ammonia and urea who must now disclose electricity-based data for compliance. With the EU proposing to expand these rules to organic chemicals and polymers by 2028, almost the entire core product portfolio of the GPCA members could soon face carbon pricing on exports to the European market.

To better understand the implications and relationship between CBAM, product-carbon intensities, and grid emissions factors for the GCC region, a simplified example is shown below (Example 2). In its simplest form [1], under CBAM, a product’s total embedded emissions (the PCF value multiplied by its total import volume) by the prevailing EU ETS carbon price (currently €75.36 per ton CO₂e). Example 2 illustrates the scale of the CBAM exposure to GCC exporters across the decarbonization scenarios (as outlined in Table 1 and Table 2).

[1] This article ignores the free allocation period in the early roll-out of CBAM as well as consideration for avoidance of double taxation if the exporting market already has a domestic carbon tax in place that applies to the producer.

Key takeaways

Product-carbon footprints are rapidly becoming one of the most consequential metrics a GCC producer can report, influencing CBAM liability, procurement decisions, and market access in carbon-regulated economies. Grid decarbonization will reduce the electricity component over time, but that trajectory is passive and country dependent. The PCF, however, can be actively managed. Producers who understand and reduce their full emissions profile, across electricity, combustion, and upstream inputs, will be better positioned with regulators, buyers, and competitors alike.

The third and final article in this series will dissect this topic further by looking at how companies can use contractual mechanisms like power purchase agreements or energy attribute certificates (e.g. I-RECs) to report their Scope 2 emissions for life-cycle assessments, environmental product declarations, and product carbon footprints (particularly in light of the evolving requirements of the GHG Protocol, ISO 14067, and SBTi standards), while also looking at the limitations for doing so with CBAM.